Acta mathematica scientia,Series A ›› 2026, Vol. 46 ›› Issue (1): 343-358.

• Original article • Previous Articles Next Articles

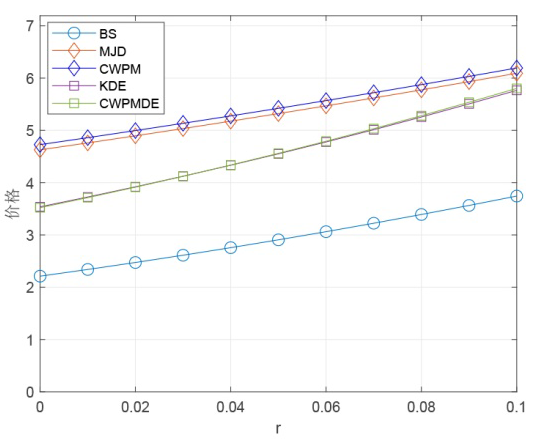

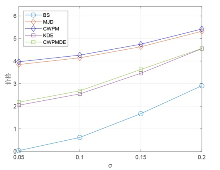

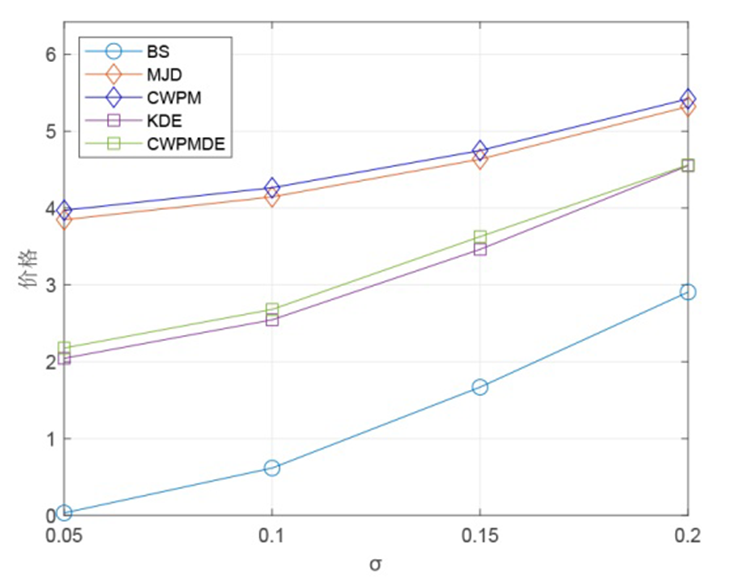

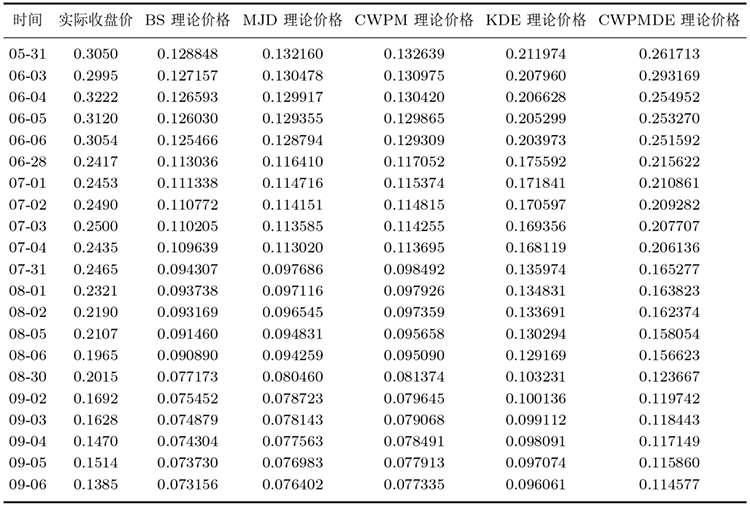

European Maximal Call Options Pricing in a Multidimensional Jump Diffusion Market Model Under a Fuzzy Environment

Hongwei Liu1,2,3, Yajun Wang1, Pengcheng Ma1,*( )

)

- 1School of Mathematics and Computing Science, Guilin University of Electronic Technology, Nanning Guilin 541004

2Guangxi Colleges and Universities Key Laboratory of Data Analysis and Computation, Nanning Guilin 541004

3Center for Applied Mathematics of Guangxi (GUET), Nanning Guilin 541004

-

Received:2024-09-11Revised:2025-04-15Online:2026-02-26Published:2026-01-19 -

Contact:Pengcheng Ma E-mail:lhw_28@163.com -

Supported by:Science and Technology Project of Guangxi(Guike AD25069086);Guangxi Natural Science Foundation(2025GXNSFAA069661)

CLC Number:

- O211

Cite this article

Hongwei Liu, Yajun Wang, Pengcheng Ma. European Maximal Call Options Pricing in a Multidimensional Jump Diffusion Market Model Under a Fuzzy Environment[J].Acta mathematica scientia,Series A, 2026, 46(1): 343-358.

share this article

Add to citation manager EndNote|Reference Manager|ProCite|BibTeX|RefWorks

"

|

"

|

"

|

"

"

"

|

"

| [1] |

Merton R C. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics, 1976, 3(1/2): 125-144

doi: 10.1016/0304-405X(76)90022-2 |

| [2] |

Kou S G. A jump diffusion model for option pricing. Management Science, 2002, 48(8): 1086-1101

doi: 10.1287/mnsc.48.8.1086.166 |

| [3] | 邓国和, 杨向群. 随机波动率与双指数跳扩散组合模型的美式期权定价. 应用数学学报, 2009, 32(2): 236-255 |

| Deng G H, Yang X Q. Valuation of american option in a double exponential jump-diffusion model with stochastic volatility. Acta Mathematicae Applicatae Sinica, 2009, 32(2): 236-255 | |

| [4] |

周伟, 何建敏, 余德建. 随机跳变广义双指数分布下的双重跳跃扩散模型及应用. 系统工程理论与实践, 2013, 33(11): 2746-2756

doi: 10.12011/1000-6788(2013)11-2746 |

| Zhou W, He J M, Yu D J. Double-jump diffusionmodel based on the generalized double exponential distribution of the random jump and its application. Systems Engineering Theory and Practice, 2013, 33(11): 2746-2756 | |

| [5] |

Zadeh L A. Fuzzy sets. Information and Control, 1965, 8(3): 338-353

doi: 10.1016/S0019-9958(65)90241-X |

| [6] | Puri M L, Ralescu D A, Zadeh L. Fuzzy random variables. Readings in fuzzy sets for intelligent systems. Morgan Kaufmann, 1993, 265-271 |

| [7] |

Carlsson C, Fullér R. A fuzzy approach to real option valuation. Fuzzy Sets and Systems, 2003, 139(2): 297-312

doi: 10.1016/S0165-0114(02)00591-2 |

| [8] |

Yoshida Y. The valuation of European options in uncertain environment. European Journal of Operational Research, 2003, 145(1): 221-229

doi: 10.1016/S0377-2217(02)00209-6 |

| [9] |

Yoshida Y, Yasuda M, Nakagami J I, Kurano M. A new evaluation of mean value for fuzzy numbers and its application to American put option under uncertainty. Fuzzy Sets and Systems, 2006, 157(19): 2614-2626

doi: 10.1016/j.fss.2003.11.022 |

| [10] |

Zhang L H, Zhang W G, Xu W J, et al. The double exponential jump diffusion model for pricing European options under fuzzy environments. Economic Modelling, 2012, 29(3): 780-786

doi: 10.1016/j.econmod.2012.02.005 |

| [11] |

Xu W, Wu C, Xu W, Li H. A jump-diffusion model for option pricing under fuzzy environments. Mathematics and Economics, 2009, 44(3): 337-344

doi: 10.1016/j.insmatheco.2008.09.003 |

| [12] |

Wu H C. Pricing European options based on the fuzzy pattern of Black-Scholes formula. Computers and Operations Research, 2004, 31(7): 1069-1081

doi: 10.1016/S0305-0548(03)00065-0 |

| [13] |

Muzzioli S, Torricelli C. A multiperiod binomial model for pricing options in a vague world. Journal of Economic Dynamics and Control, 2004, 28(5): 861-887

doi: 10.1016/S0165-1889(03)00060-5 |

| [14] |

Chrysafs K A, Papadopoulos B K, Papaschinopoulos G. On the fuzzy diference equations of finance. Fuzzy Sets and Systems, 2008, 159(24): 3259-3270

doi: 10.1016/j.fss.2008.06.007 |

| [15] |

Liu W, Li S. European option pricing model in a stochastic and fuzzy environment. Applied Mathematics-A Journal of Chinese Universities, 2013, 28(3): 321-334

doi: 10.1007/s11766-013-3030-0 |

| [16] |

Lee C F, Tzeng G H, Wang S Y. A fuzzy set approach for generalized CRR model: An empirical analysis of S and P 500 index options. Review of Quantitative Finance and Accounting, 2005, 25: 255-275

doi: 10.1007/s11156-005-4767-1 |

| [17] |

Nowak P, Romaniuk M. Computing option price for Levy process with fuzzy parameters. European Journal of Operational Research, 2010, 201(1): 206-210

doi: 10.1016/j.ejor.2009.02.009 |

| [18] | Appadoo S S, Bector C R. Binomial option pricing model using O(2, 2) trapezoidal fuzzy numbers. In Proc Alliance Study Adoption Culture Conf, 2005, 46-58 |

| [19] | 秦学志, 吴冲锋. 具有交易费用的或有要求权的模糊估价方法. 模糊系统与数学, 2003, 17(1): 73-76 |

| Qin X Z, Wu C F, Fuzzy credit pricing method for contingent claims with transaction cost. Fuzzy Systems and Mathematics, 2003, 17(1): 73-76 | |

| [20] | 詹惠蓉, 彭龙. 基于加权可能性均值的亚式期权模糊定价. 数学的实践与认识, 2011, 41(3): 78-85 |

| Zhan H R, Peng L. The fuzzy pricing of asian options based on weighted possibilistic mean. Mathematics in Practice and Theory, 2011, 41(3): 78-85 | |

| [21] | 马勇, 张卫国, 刘勇军, 等. 模糊随机环境中的欧式障碍期权定价. 系统工程学报, 2012, 27(5): 641-647 |

| Ma Y, Zhang W G, Liu Y J, et al. Pricing european barrier options in fuzzy and stochastic environment. Journal of Systems Engineering, 2012, 27(5): 641-647 | |

| [22] |

Fullér R, Majlender P. On weighted possibilistic mean and variance of fuzzy numbers. Fuzzy sets and Systems, 2003, 136(3): 363-374

doi: 10.1016/S0165-0114(02)00216-6 |

| [23] |

Malinowski M T. Strong solutions to stochastic fuzzy differential equations of Ito type. Mathematical and Computer Modelling, 2012, 55: 918-928

doi: 10.1016/j.mcm.2011.09.018 |

| [24] |

Malinowski M T. Some properties of strong solutions to stochastic fuzzy differential equations. Information Sciences, 2013, 252: 62-80

doi: 10.1016/j.ins.2013.02.053 |

| [25] | Shreve S E. Stochastic Calculus for Finance II:Continuous-time Models. New York: Springer, 2004 |

| [1] | Qinwen Li, Shoujiang Zhao. Sharp Large Deviations of the Non-Stationary Ornstein-Uhlenbeck Process with Linear Drift [J]. Acta mathematica scientia,Series A, 2026, 46(1): 305-317. |

| [2] | Leilei Gan, Yifei Hao, Yingzhe Wang. Algebraic Degeneration of One-Dimension Non-Recurrent Diffusion Processes [J]. Acta mathematica scientia,Series A, 2026, 46(1): 270-285. |

| [3] | Liang Qing. Existence, Uniqueness and Stability of the Global Solutions to Two Classes of Pantogragh Stochastic Functional Differential Equations with Markovian Switching [J]. Acta mathematica scientia,Series A, 2025, 45(4): 1184-1205. |

| [4] | Zhu Zhifeng, Zhou Junchao, Huang Hong. Harris Recurrence of Continuous-Time Markov Process on General State Space [J]. Acta mathematica scientia,Series A, 2025, 45(4): 1245-1254. |

| [5] | Wen Yuzhen, Wang Shaolin. Stackelberg Stochastic Differential Game of Insurer and Reinsurer Under Mean-Variance Framework [J]. Acta mathematica scientia,Series A, 2025, 45(4): 1327-1353. |

| [6] | Liu Yu, Chen Guanggan, Li Shuyong. Nonlinear Stability of Traveling Waves for Stochastic Kuramoto-Sivashinsky Equation [J]. Acta mathematica scientia,Series A, 2025, 45(3): 790-806. |

| [7] |

Chen Yating, Liu Haiyan, Chen Mi.

|

| [8] | Han Qi, Gou Lijie, Wang Shuai, Bai Ning, Wang Huan, Han Yanan. Entanglement Testing Based on Affine Mapping [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1136-1143. |

| [9] | Lu Yingyin, Zhang Wenjing, Guo Jinhui. Joint Behavior of Point Process of Clusters and Partial Sum for a Gaussian Triangular Array [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1311-1318. |

| [10] | Fan Tianjiao, Feng Lichao, Yang Yanmei. Generalization of Inequality and Its Application in Additive Time-Varying Delay Systems [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1335-1351. |

| [11] | Wang Qiufen, Zhang Shuwen. Stochastic Predator-Prey System with Fear Effect and Holling-Type III Functional Response [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1380-1391. |

| [12] | Yang Hong, Zhang Xiaoguang. A Stochastic SIS Epidemic Model on Simplex Complexes [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1392-1399. |

| [13] | Wang Yankai, Peng Xingchun. Time-Consistent Risk Control and Investment Strategies With Transaction Costs [J]. Acta mathematica scientia,Series A, 2024, 44(5): 1400-1414. |

| [14] | Wang Jiaxi, Mao Mingzhi. The Asymptotic Behaviors for Parameter Estimation of Stochastic Functional Differential Equations [J]. Acta mathematica scientia,Series A, 2024, 44(3): 746-760. |

| [15] | Zhang Cong, Ding Yiming. Non-stationarity Measurement Based on Law of Iterated Logarithm [J]. Acta mathematica scientia,Series A, 2023, 43(6): 1855-1868. |

|

||