数学物理学报 ›› 2026, Vol. 46 ›› Issue (3): 1255-1269.

模糊厌恶下考虑巨灾债券发行的最优投资与风险管理策略

刘兵*( ), 钱通(), 李鹏()

), 钱通(), 李鹏()

南京财经大学金融学院 南京 210023

-

收稿日期:2025-03-06修回日期:2025-10-21出版日期:2026-06-26发布日期:2026-06-16 -

通讯作者:刘兵 E-mail:liubingsdly@sina.com;qiantong666@sina.cn;pengli1@unfe.edu.cn -

作者简介:钱通, E-mail:qiantong666@sina.cn;

李鹏, E-mail:pengli1@unfe.edu.cn -

基金资助:国家自然科学基金(12101300);国家自然科学基金(12401614)

Optimal Investment and Risk Management Strategies Considering Catastrophe Bond Issuance Under Ambiguity Aversion

Bing Liu*(), Tong Qian(), Peng Li()

School of Finance Nanjing University of Finance and Economics Nanjing 210023

-

Received:2025-03-06Revised:2025-10-21Online:2026-06-26Published:2026-06-16 -

Contact:Bing Liu E-mail:liubingsdly@sina.com;qiantong666@sina.cn;pengli1@unfe.edu.cn -

Supported by:NSFC(12101300);NSFC(12401614)

摘要:

气候与环境的变化加剧了自然灾害的频发态势, 对保险公司的风险管理造成了严峻挑战. 因此, 探究保险公司在面临自然灾害等巨灾风险时的最优投资与再保险策略极其必要. 论文创新性地融合了巨灾债券发行和模型不确定性两个因素到传统的最优投资-再保险策略研究中. 通过运用随机控制理论和动态规划方法, 得出了最优投资-再保-巨灾债券发行策略的解析解. 通过数值模拟, 揭示了保险公司发行巨灾债券后最优投资-再保险策略的动态变化特征. 同时, 探讨了市场相关性、模糊厌恶系数等关键参数对策略选择的敏感性和经济影响. 研究结果表明, 巨灾债券发行 (购买) 可以有效替代再保险, 发行 (购买) 量增加时, 再保险购买减少; 巨债券和保险市场相关性的增强可以促使保险公司减少风险投资、增加巨灾债券持有; 不确定性环境下, 保险公司将更加依赖巨灾债券进行风险管理, 并倾向于投资确定性高的市场; 同时随着资金增加, 投资策略趋于保守.

中图分类号:

- O29

引用本文

刘兵, 钱通, 李鹏. 模糊厌恶下考虑巨灾债券发行的最优投资与风险管理策略[J]. 数学物理学报, 2026, 46(3): 1255-1269.

Bing Liu, Tong Qian, Peng Li. Optimal Investment and Risk Management Strategies Considering Catastrophe Bond Issuance Under Ambiguity Aversion[J]. Acta mathematica scientia,Series A, 2026, 46(3): 1255-1269.

表1

模型参数"

|

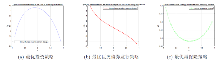

图1

确定模型下 $\rho$ 对最优投资-再保险-巨灾债券发行策略的影响"

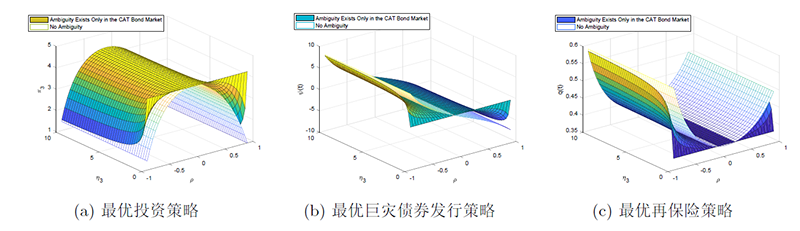

图2

模型不确定只存在于巨灾债券市场与确定模型下相关策略的对比"

图3

模型不确定只存在于巨灾债券市场与三市场均存在模型不确定下相关策略的对比"

图4

模型不确定下保险公司的资金 $x$ 对相关策略的影响"

| [1] |

Browne S. Optimal investment policies for a firm with a random risk process: exponential utility and minimizing the probability of ruin. Mathematics of Operations Research, 1995, 20 (4): 937-958

doi: 10.1287/moor.20.4.937 |

| [2] |

Schmidli H. Optimal proportional reinsurance policies in a dynamic setting. Scandinavian Actuarial Journal, 2001, 2001 (1): 55-68

doi: 10.1080/034612301750077338 |

| [3] |

Promislow S D, Young V R. Minimizing the probability of ruin when claims follow Brownian motion with drift. North American Actuarial Journal, 2005, 9 (3): 109-128

doi: 10.1080/10920277.2005.10596229 |

| [4] |

Yang H, Zhang L. Optimal investment for insurer with jump-diffusion risk process. Insurance: Mathematics and Economics, 2005, 37 (3): 615-634

doi: 10.1016/j.insmatheco.2005.06.009 |

| [5] |

Lin X, Li Y F. Optimal reinsurance and investment for a jump diffusion risk process under the CEV model. North American Actuarial Journal, 2011, 15 (3): 417-431

doi: 10.1080/10920277.2011.10597628 |

| [6] |

Li D, Zeng Y, Yang H. Robust optimal excess-of-loss reinsurance and investment strategy for an insurer in a model with jumps. Scandinavian Actuarial Journal, 2018, 2018 (2): 145-171

doi: 10.1080/03461238.2017.1309679 |

| [7] |

Bai L, Guo J. Optimal proportional reinsurance and investment with multiple risky assets and no-shorting constraint. Insurance: Mathematics and Economics, 2008, 42 (3): 968-975

doi: 10.1016/j.insmatheco.2007.11.002 |

| [8] |

Jin Z, Xu Z Q, Zou B. A perturbation approach to optimal investment, liability ratio, and dividend strategies. Scandinavian Actuarial Journal, 2022, 2022 (2): 165-188

doi: 10.1080/03461238.2021.1938199 |

| [9] | 张帅琪, 刘国欣. 复合 Poisson 模型带比例与固定交易费用的最优分红与注资. 中国科学: 数学, 2012, 42 (8): 827-843 |

| Zhang S Q, Liu G X. Optimal dividend payment and capital injection of the compound Poisson risk model with both proportional and fixed costs Sci Sin Math, 2012, 42 (8): 827-843 (in Chinese). | |

| [10] |

Yao D, Wang R, Xu L. Optimal dividend and capital injection strategy with fixed costs and restricted dividend rate for a dual model. Journal of Industrial and Management Optimization, 2014, 10 (4): 1235-1259

doi: 10.3934/jimo.2014.10.1235 |

| [11] |

Zhou M, Yuen K C. Portfolio selection by minimizing the present value of capital injection costs. ASTIN Bulletin, 2015, 45 (1): 207-238

doi: 10.1017/asb.2014.22 |

| [12] | 李鹏, 周明, 孟辉. 脉冲和正则控制下的最优注资: 一种混合策略. 中国科学: 数学, 2018, 48 (4): 565-578 |

| Li P, Zhou M, Meng H. Optimal stochastic impulse and regular control for capital injections: A hybrid strategy Sci Sin Math, 2018, 48 (4): 565-578 (in Chinese). | |

| [13] |

陈树敏, 曾燕, 谷爱玲. R $\& $ D 企业最优技术投资与分红策略研究. 系统工程理论与实践, 2019, 39 (6): 1394-1406

doi: 10.12011/1000-6788-2018-0276-13 |

| Chen M, Zeng Y, Gu A L. Optimal technology investment-dividend strategy for a R$\&$D firm. Systems Engineering-Theory $\&$ Prectice, 2019, 39 (6): 1394-1406 | |

| [14] |

Guan C, Xu Z Q, Zhou R. Dynamic optimal reinsurance and dividend payout in finite time horizon. Mathematics of Operations Research, 2023, 48 (1): 544-568

doi: 10.1287/moor.2022.1276 |

| [15] |

姚海祥, 伍慧玲, 曾燕. 不确定终止时间和通货膨胀影响下风险资产的最优投资策略, 系统工程理论与实践, 2014, 34 (5): 1089-1099

doi: 10.12011/1000-6788(2014)5-1089 |

| Yao H X, Wu H L, Zeng Y. Optimal investment strategy for risky assets under uncertain time-horizon and inflation. Systems Engineering-Theory $\&$ Prectice, 2014, 34 (5): 1089-1099 | |

| [16] |

Guan G, Liang Z. Optimal reinsurance and investment strategies for insurer under interest rate and inflation risks. Insurance: Mathematics and Economics, 2014, 55 : 105-115

doi: 10.1016/j.insmatheco.2014.01.007 |

| [17] |

伍慧玲, 董洪斌. 带有通货膨胀风险和随机收入的确定缴费养老金计划. 系统工程理论与实践, 2016, 36 (3): 545-558

doi: 10.12011/1000-6788(2016)03-0545-14 |

| Wu H L, Dong H B. Multi-period mean-variance defined contribution pension management with inflation and stochastic income. Systems Engineering-Theory $\&$ Prectice, 2016, 36 (3): 545-558 | |

| [18] | 曾燕, 黄金波. 基于均值-AS 模型的资产配置. 管理科学学报, 2016, 19 (2): 95-108 |

| Zeng Y, Huang J B. Asset allocation based on mean-AS model. Journal of Management Science in China, 2016, 19 (2): 95-108 | |

| [19] |

Yao H X, Li Z F, Li D. Multi-period mean-variance portfolio selection with stochastic interest rate and uncontrollable liability. European Journal of Operational Research, 2016, 252 (3): 837-851

doi: 10.1016/j.ejor.2016.01.049 |

| [20] |

Yang Y, Wang G J, Yao J. Time-consistent reinsurance-investment games for multiple mean-variance insurers with mispricing and default risks. Insurance: Mathematics and Economics, 2024, 114 : 79-107

doi: 10.1016/j.insmatheco.2023.11.004 |

| [21] |

Liang Z, Yuen K C. Optimal dynamic reinsurance with dependent risks: variance premium principle. Scandinavian Actuarial Journal, 2016, 2016 (1): 18-36

doi: 10.1080/03461238.2014.892899 |

| [22] | Wang W Y, Zhang Z M. Computing the Gerber-Shiu function by frame duality projection. Scandinavian Actuarial Journal, 2019, 2019 (4): 291-307 |

| [23] |

Yuan Y, Han X, Liang Z, Yuen K C. Optimal reinsurance-investment strategy with thinning dependence and delay factors under mean-variance framework. European Journal of Operational Research, 2023, 311 (2): 581-595

doi: 10.1016/j.ejor.2023.05.023 |

| [24] |

Rong X, Yan Y, Zhao H. Optimal reinsurance and investment problem with multiple risky assets and correlation risk for an insurer under the Ornstein-Uhlenbeck model. Communications in Statistics-Theory and Methods, 2024, 53 (8): 2689-2714

doi: 10.1080/03610926.2022.2148470 |

| [25] |

Shen Y, Zeng Y. Optimal investment-reinsurance strategy for mean-variance insurers with square-root factor process. Insurance: Mathematics and Economics, 2015, 62 (3): 118-137

doi: 10.1016/j.insmatheco.2015.03.009 |

| [26] | Liu B, Meng H, Zhou M. Optimal investment and reinsurance policies for an insurer with ambiguity aversion. North American Journal of Economics and Finance, 2021, 55 : Art 101303 |

| [27] |

Dong X, Rong X M, Zhao H. Non-zero-sum reinsurance and investment game with non-trivial curved strategy structure under Ornstein-Uhlenbeck process. Scandinavian Actuarial Journal, 2023, 2023 (6): 565-597

doi: 10.1080/03461238.2022.2139631 |

| [28] |

Anderson E, Hansen L P, Sargent T. A quartet of semigroups for model specification, robustness, prices of risk, and model detection. Journal of the European Economic Association, 2003, 1 (1): 68-123

doi: 10.1162/154247603322256774 |

| [29] |

Yi B, Li Z, Viens F G, Zeng Y. Robust optimal control for an insurer with reinsurance and investment under heston's stochastic volatility model. Insurance Mathematics and Economics, 2013, 53 (3): 601-614

doi: 10.1016/j.insmatheco.2013.08.011 |

| [30] |

Hu D, Chen S, Wang H. Robust reinsurance contracts with uncertainty about jump risk. European Journal of Operational Research, 2018, 266 (3): 1175-1188

doi: 10.1016/j.ejor.2017.10.061 |

| [31] |

Bayraktar E, Zhang Y. Minimizing the probability of lifetime ruin under ambiguity aversion. SIAM Journal on Control and Optimization, 2015, 53 (1): 58-90

doi: 10.1137/140955999 |

| [32] |

Sun Z, Zheng X, Zhang X. Robust optimal investment and reinsurance of an insurer under variance premium principle and default risk. Journal of Mathematical Analysis and Applications, 2017, 446 (2): 1666-1686

doi: 10.1016/j.jmaa.2016.09.053 |

| [33] | 李仲飞, 袁子甲. 参数不确定性下资产配置的动态均值-方差模型. 管理科学学报, 2010, 13 (12): 1-9 |

| Li Z F, Yuan Z J. A dynamic mean-variance model of portfolio selection under parameter uncertainty. Journal of management science in China, 2010, 13 (12): 1-9 | |

| [34] | 宫晓琳, 杨淑振, 胡金焱, 张宁. 非线性期望理论与基于模型不确定性的风险度量. 经济研究, 2015, 578 (11): 135-149 |

| Gong X L, Yang S Z, Hu J Y, Zhang N. Non-linear expectation theory and risk measurement based on model ambiguity. Economic Research Journal, 2015, 578 (11): 135-149 | |

| [35] |

Zeng Y, Li D, Gu A. Robust equilibrium reinsurance-investment strategy for a mean-variance insurer in a model with jumps. Insurance Mathematics and Economics, 2016, 66 : 138-152

doi: 10.1016/j.insmatheco.2015.10.012 |

| [36] |

Zheng X X, Zhou J M, Sun Z Y. Robust optimal portfolio and proportional reinsurance for an insurer under a CEV model. Insurance: Mathematics and Economics, 2016, 67 : 77-87

doi: 10.1016/j.insmatheco.2015.12.008 |

| [37] |

刘兵, 周明. 模糊厌恶下的最优投资与最优保费策. 系统工程理论与实践, 2020, 40 (7): 1707-1720

doi: 10.12011/1000-6788-2019-0365-14 |

| Liu B, Zhou M. Optimal investment and premium policies with ambiguity aversion. Systems Engineering-Theory $\&$ Practice, 2020, 40 (7): 1707-1720 | |

| [38] | 孟辉, 魏丽, 周明. 模糊厌恶下保险人的鲁棒再保险策略. 中国科学: 数学, 2021, 51 (11): 1791-1818 |

| Meng H, Wei L, Zhou M. Robust reinsurance strategy under ambiguity-averse Sci Sin Math, 2021, 51 (11): 1791-1818 (in Chinese). | |

| [39] |

王佩, 李仲飞, 张玲. 不完全信息和模糊厌恶下 DC 型养老金最优投资策略. 运筹与管理, 2022, 31 (6): 125-132

doi: 10.12005/orms.2022.0192 |

| Wang P, Li Z F, Zhang L. Optimal investment strategy for a DC pension with incomplete information and ambiguity aversion. Operations Research and Mangement Science, 2022, 31 (6): 125-132 | |

| [40] |

Liu B, Zhang L, Zhou M. Portfolio selections for insurers with ambiguity aversion: minimizing the probability of ruin. Applied Economics, 2024, 56 (12): 1423-1439

doi: 10.1080/00036846.2023.2176453 |

| [41] | Nell M, Richter A. Improving risk allocation through cat bonds. The Geneva Papers on Risk and Insurance, 2004, 29 : 183-201 |

| [42] |

Bauerle N. Traditional versus non-traditional reinsurance in a dynamic setting. Scandinavian Actuarial Journal, 2004, 2004 (5): 355-371

doi: 10.1080/03461230310016983 |

| [43] |

Li Y, Wei P, Zhang J. Robust risk control with reinsurance and CAT bonds. North American Actuarial Journal, 2025, 29 (3): 713-738

doi: 10.1080/10920277.2025.2455474 |

| [44] | Fleming W H, Soner M. Controlled Markov Processes and Viscosity Solutions. New York: Springer, 2006 |

| [1] | 刘红卫, 王亚军, 马鹏程. 模糊环境下多维跳跃扩散市场模型的欧式极大看涨期权定价[J]. 数学物理学报, 2026, 46(1): 343-358. |

| [2] | 赵玉莹,温玉珍. 模糊厌恶下最小Drawdown概率的最优投资再保险策略[J]. 数学物理学报, 2021, 41(4): 1147-1165. |

| [3] | 熊才权,李煊,邓娜,閤大海. 基于IBIS的协商对话框架及共识评价方法[J]. 数学物理学报, 2019, 39(5): 1213-1227. |

| [4] | 熊君, 李俊民, 何超. 一阶双曲型偏微分方程的模糊边界控制[J]. 数学物理学报, 2017, 37(3): 469-477. |

| [5] | 肖爽, 蹇明, 陈爱香, 蹇贝. 模糊环境中跳扩散模型下带交易费用的期权定价方法[J]. 数学物理学报, 2015, 35(1): 118-130. |

| [6] | 庞志峰, 杨余飞, 丁立新, 谢德宣. 解非负约束图像去模糊问题的积极集方法[J]. 数学物理学报, 2013, 33(1): 134-144. |

| [7] | 蹇明, 边潇男. 模糊环境下带交易费用的权证定价模型——纪念李国平院士吴新谋教授诞辰100周年[J]. 数学物理学报, 2010, 30(5): 1254-1262. |

| [8] | 陈世鸿, 彭蓉. 模糊逻辑语言FLL的并行计算模型FPCM[J]. 数学物理学报, 2002, 22(1): 48-54. |

| [9] | 侯振挺, 郭先平. 非齐次马氏决策过程的齐次化[J]. 数学物理学报, 1997, 17(4): 432-438. |

|

||