1 引言

保险公司作为金融体系的关键支柱, 通过收取保费并建立风险共担机制, 为投保人提供风险补偿. 同时, 保险公司还通过保费的投资运作, 对资本市场的流动性和稳定性产生深远影响. 2024 年 9 月,《国务院关于加强监管防范风险推动保险业高质量发展的若干意见》(新国十条) 明确指出要丰富巨灾保险保障形式, 研究探索巨灾债券, 合理运用再保险分散风险, 发挥保险资金长期投资优势等.

事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14]); 通胀风险下的投资组合问题 (文献 [15 18]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27]) 等.

然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40]) 等.

特别地, 巨灾债券作为一种创新的风险管理工具, 允许保险公司将部分巨灾风险转移至资本市场, 从而降低风险分散的成本. 然而, 在现有的文献中考虑巨灾债券的研究相对较少. 据我们所知的相关研究有, Nell-Richter[41 ] 较早地研究了巨灾债券与再保险之间的替代关系, 发现巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力. Bauerle[42 ] 则在一个随机风险收入过程下研究了保险公司购买比例再保险和发行巨灾债券的风险管理策略. Li-Wei[43 ] 探讨了模糊厌恶下的巨灾债券发行和再保险策略问题. 研究表明, 巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力, 并能在随机风险收入过程下为保险公司提供有效的风险管理策略.

因此, 本文以最小化保险公司的破产概率为目标将巨灾债券发行和模型不确定性两个因素引入到传统的最优投资-再保险策略研究中, 旨在为保险公司提供更加全面和精准的风险管理工具, 以应对日益复杂多变的市场环境和自然灾害风险.

首先, 巨灾债券作为一种创新的风险转移工具, 其发行能够帮助保险公司有效分散和转移巨灾风险, 增强公司的偿付能力和财务稳定性. 通过将巨灾风险与资本市场相连, 巨灾债券不仅能够为保险公司提供额外的资金来源, 还能够在灾害发生时, 通过债券市场的反应机制, 实现风险的快速分散和转移. 其次, 模型不确定性是保险公司在制定投资策略时不可忽视的重要因素. 由于市场环境、经济条件和自然灾害等因素的复杂性和不确定性, 传统的风险模型往往难以准确预测和评估风险. 因此, 本文将在研究中考虑模型不确定性, 探讨其对保险公司最优投资-再保险-巨灾发行策略的影响. 通过构建包含模型不确定性的风险优化模型, 帮助保险公司更好地理解和应对模型不确定性带来的风险, 提高风险管理决策的准确性和稳健性. 最后, 本文将结合数值分析, 对引入巨灾债券和模型不确定性的最优投资-再保险策略进行深入研究. 通过对比分析不同策略下的风险管理和投资效果, 为保险公司提供具体的策略建议和实践指导, 以助其更好地应对风险挑战, 实现稳健发展.

本文其余部分结构安排如下: 第二章为模型的详细构建过程; 第三章介绍最优策略的求解; 第四章为数值模拟, 讨论巨灾债券对再保险的替代作用、最优投资以及风险管理策略的敏感性分析; 第五章是结论.

2 模型设定

假设 $(\Omega, \mathcal{F}, \{\mathcal{F}_{t}\}_{t\in[T]}, \mathbb{P})$ $\{\mathcal{F}_{t}\}_{t\in[T]}$ $t$ $t$ $\{B_1(t);t\geq0\}$ $\{B_2(t);t\geq0\}$ $\{B_3(t);t\geq0\}$ $\mathbb{P}$

本文用古典风险模型 ($Cramér - Lundberg$ ) 来刻画保险公司的盈余过程 $\{M(t); t\geq0\}$

其中 $x_{0}>0$ $C(t)$ $t$ $\{N(t),t\geq0\}$ $\lambda$ $t$ $Y_{i}, i=1,2,\cdots$ $i$ $\{N(t), t\geq0\}$ $0<EY_i<\infty$ $0<EY_i^2<\infty$ $\mu= EY_i$ $\sigma^{2}=EY_i^{2}$ $\theta_{1}$ . 因此, 可以得到

此外, 保险公司可以通过购买比例再保险来控制其保险风险敞口. 假设在时刻 $t$ $q(t)\in [0,1]$ $1-q(t)\in [0,1]$ $\theta_{2}$ $(\theta_{2}>\theta_{1}>0)$ $C_{1}(t)$ $C_{1}(t)=(1+\theta_{2})(1-q(t))\lambda EY_i t$ .

特别地, 保险公司不仅能够借助再保险机制实现风险的转移, 还可以通过发行 (或购入) 巨灾债券这一金融工具来有效降低其风险敞口. 假设保险公司在 $t$ $\psi(t)$ $\psi(t)<0$ $Y$ $K$ $\overline{k}$ $\varphi$ $K_{1}, K_{2}, K_{3},\cdots$ $Y_{1}, Y_{2}, Y_{3},\cdots$

条件概率随着 $y$ $p=E[p(Y)]$ $Y$ $\lambda p\varphi(1+\theta_{3})$ $\theta_{3}$ $\theta_{2}>\theta_{3}$

其中${1}_{\{K_{i}\geq\overline{k}\}}$

显然, 保险市场和巨灾债券市场存在相关性, 用 $\rho$ $ Cov(B_{1}(t), B_{3}(t))=\rho t $ . 由高斯线性回归, 则有

其中 $B_{4}(t)$ $B_{1}(t)$ $(\Omega^4, \mathcal{F}^4, \mathbb{P}^4)$ .

$\begin{aligned}\mathrm{d} M(t)= & \mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\lambda p \varphi \theta_{3} \psi(t) \mathrm{d} t+(q(t) \sigma \sqrt{\lambda}+\sqrt{\lambda p} \varphi \rho \psi(t)) \mathrm{d} B_{1}(t) \\& +\sqrt{\lambda p} \varphi \psi(t) \sqrt{1-\rho^{2}} \mathrm{~d} B_{4}(t), \quad M(0)=x_{0}\end{aligned}$

进一步, 假设保险公司可以投资于风险资产、无风险资产, 无风险资产的价格过程为${\text d}S_{0}(t)=r S_{0}(t) {\text d}t,$ $r>0$

其中 $\alpha_{1}>r$ $\beta_{1}$ $B_{2}(t)$ $B_{2}(t)$ $(\Omega^{2}, \mathcal{F}^{2}, \mathbb{P}^{2})$

令 $X_{t}$ $t$ $\pi_{3t}$ $t$ $X(t)-\pi_{3t}$ $t$

(2.1) $\begin{aligned}\mathrm{d} X_{t}^{\pi_{3}}= & \left(X(t)^{\pi_{3}} r+\pi_{3 t}\left(\alpha_{1}-r\right)+\mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\lambda p \varphi \theta_{3} \psi(t)\right) \mathrm{d} t \\& +(q(t) \sigma \sqrt{\lambda}+\psi(t) \sqrt{\lambda p} \varphi \rho) \mathrm{d} B_{1}(t)+\pi_{3 t} \beta_{1} \mathrm{~d} B_{2}(t) \\& +\sqrt{\lambda p} \varphi \sqrt{1-\rho^{2}} \psi(t) \mathrm{d} B_{4}(t), \quad X(0)^{\pi_{3}}=x_{0}\end{aligned}$

显然, 上述模型建立在概率空间 $(\Omega,\mathcal{F},\mathbb{P})$ $(\Omega^{1}\times\Omega^{2}\times\Omega^{4},\mathcal{F}^{1}\times\mathcal{F}^{2}\times\mathcal{F}^{4}, \mathbb{P}^{1} \times \mathbb{P}^{2} \times \mathbb{P}^{4})$ $(\Omega,\mathcal{F},\mathbb{P})$ $(\Omega^1,\mathcal{F}^1,\mathbb{P}^1)$ $\{\mathcal{F}^1_t\}$ $(\Omega^2, \mathcal{F}^2, \mathbb{P}^2)$ $\{\mathcal{F}^2_t\}$ $(\Omega^4,\mathcal{F}^4,\mathbb{P}^4)$ $\{\mathcal{F}^4_t\}$ $B_1(t)$ $B_2(t)$ $B_4(t)$

由于数据限制和技术水平的局限性, 原始的概率测度 $\mathbb{P}$

进一步地, 定义一个替代概率测度族 $\mathcal{Q}$ $\mathbb{P}$ $\mathbb{Q}$ . 这里的“等价”意味着这些替代测度在保持市场模型基本结构不变的前提下, 对原始概率测度进行了合理的替代. 通过这样的设定, 我们旨在找到一个既能够反映保险公司主观信念, 又能够保持市场模型一致性的替代概率测度. 我们用 $\mathbb{Q}^{1}$ $\mathbb{Q}^{2}$ $\mathbb{Q}^{4}$ $\mathbb{P}^{1}$ $\mathbb{P}^{2}$ $\mathbb{P}^{4}$

对任意 $\mathbb{Q}\in\mathcal{Q}$ $\mathbb{Q}$

$\Lambda^{\eta}(t)$ $\{\mathcal{F}_t\}$ $\mathbb{P}$ - 鞅; $o(t)$ $u(t)$ $w(t)$ $\Lambda^{\eta}(t)$ $\{\mathcal{F}_{t}\}$

根据Girsanov定理, 在概率测度 $\mathbb{Q}^{1}$ $\mathbb{Q}^{2}$ $\mathbb{Q}^{4}$

$\left\{\begin{array}{l}\mathrm{d} B_{1}(t)=o(t) \mathrm{d} t+\mathrm{d} B_{1}^{\mathbb{Q}^{1}}(t), \\\mathrm{d} B_{2}(t)=u(t) \mathrm{d} t+\mathrm{d} B_{2}^{\mathbb{Q}^{2}}(t), \\\mathrm{d} B_{4}(t)=w(t) \mathrm{d} t+\mathrm{d} B_{4}^{\mathbb{Q}^{4}}(t),\end{array}\right.$

其中 $B_{(\cdot)}^{\mathbb{Q}^{(\cdot)}}(t)$ $\mathbb{Q}^{(\cdot)}$ $\mathbb{Q}$

因此, 在概率测度 $\mathbb{Q}$

为了在替代概率测度族下研究本文的问题, 需要度量参考概率测度和替代概率测度差距, 延用通用的方法, 本文采用相对熵作为衡量参考概率测度与各替代概率测度之间差异的工具. 对于 $\mathbb{P}$ $\mathbb{Q}$

在保险市场维度上, 通过对比 $\mathbb{P}$ $\mathbb{Q}$ $\mathbb{P}$ $\mathbb{Q}$ $\mathbb{Q}$ $\mathbb{P}$ $\mathbb{Q}$

\noindent $\mathbb{P}^{1}$ $\mathbb{Q}^{1}$

$\mathbb{P}^{2}$ $\mathbb{Q}^{2}$

$\mathbb{P}^{4}$ $\mathbb{Q}^{4}$

因为 $B_{1}^{\mathbb{Q}^{1}}$ $B_{2}^{\mathbb{Q}^{2}}$ $B_{4}^{\mathbb{Q}^{4}}$ $\mathbb{Q}$

其中 $Z_{1}(s)=\frac{1}{2}[o(s)]^2$ $Z_{2}(s)=\frac{1}{2}[u(s)]^2$ $Z_{4}(s)=\frac{1}{2}[w(s)]^2$ .

3 最优控制问题的求解

本文探讨了在模型不确定存在的条件下, 保险公司如何通过优化投资策略、发行巨灾债券以及合理安排再保险来实现破产概率的最小化. 具体地, 记破产时刻为

其中, $a$ $a$

在建立最小化破产概率的目标函数前, 我们首先给出可容许策略的定义.

定义 3.1 定义 $\mathbb{V}$ $\pi$ $\pi = (\pi_{3},q(t),\psi(t))$

(i) 最优投资-再保险-巨灾发行策略 $\pi = (\pi_{3},q(t),\psi(t))$

其中, $\pi_{3}$ $t$ $q(t)$ $t$ $\psi(t)$ $t$

(ii) 随机微分方程 (2.1) 有唯一的强解.

本文是以最小化破产概率为目标函数, 来探讨保险公司的最优决策问题, 因此目标函数为

(3.1) $\begin{equation}\label{17} V_{2}(x)=\inf_{\pi\in\mathbb{V}}\sup_{\mathbb{Q}\in\mathcal{Q}} \bigg\{\mathbb{Q}_x\big(\tau_a^\mathbb{Q}<\infty\big)-E^\mathbb{Q}_x \bigg[\int_{0}^{\tau_a^\mathbb{Q}}\phi(V_{2}(X(s)^{\pi_3,\mathbb{Q}}))[\eta_{1} Z_{1}(s)+\eta_{2} Z_{2}(s)+\eta_{3} Z_{4}(s)]{\text d}s\bigg]\bigg\}, \end{equation}$

其中 $\mathbb{Q}_x(\cdot)=\mathbb{Q}(\cdot|X(0)^{\pi_3,\mathbb{Q}}=x)$ $E^\mathbb{Q}_x[\cdot]=E^\mathbb{Q}[\cdot|X(0)^{\pi_3,\mathbb{Q}}=x]$ $x\geq a$ $\mathbb{Q}$ $x$ $\phi(\cdot)>0$ $V_{2}(x)$ $Z_{1}(t)$ $Z_{2}(t)$ $Z_{4}(t)$ $[0,\tau_a^\mathbb{Q}]$ $\eta_{1}$ $\eta_{2}$ $\eta_{3}$ $\mathbb{P}_{1}$ $\mathbb{P}_{2}$ $\mathbb{P}_{4}$ $\mathbb{P}$ $\mathbb{V}$ $sup$ $\eta_{i}\rightarrow\infty$ $\eta_{i}\rightarrow0$

对于给定的马尔可夫控制过程 $\pi=(\pi_{3},q(t),\psi(t))$ $f(x)$

$\begin{aligned}\mathscr{A}^{\pi} f(x)= & \left(x r+\pi_{3}\left(\alpha_{1}-r\right)+\mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\psi(t) \lambda p \varphi \theta_{3}\right. \\& \left.+(q(t) \sigma \sqrt{\lambda}+\psi(t) \sqrt{\lambda p} \varphi \rho) o(t)+\pi_{3} \beta_{1} u(t)+\psi(t) \sqrt{\lambda p} \varphi \sqrt{1-\rho^{2}} w(t)\right) f^{\prime}(x) \\& +\frac{1}{2}\left((q(t) \sigma \sqrt{\lambda}+\psi(t) \sqrt{\lambda p} \varphi \rho)^{2}+\pi_{3}^{2} \beta_{1}^{2}+\psi(t)^{2} \lambda p \varphi^{2}\left(1-\rho^{2}\right)\right) f^{\prime \prime}(x),\end{aligned}$

其中 $f'(x)$ $f''(x)$ $x$ $V_2(x)$ [44 ] ) 为

(3.2) $\begin{aligned}\mathscr{A}^{\pi} f(x)= & \left(x r+\pi_{3}\left(\alpha_{1}-r\right)+\mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\psi(t) \lambda p \varphi \theta_{3}\right. \\& \left.+(q(t) \sigma \sqrt{\lambda}+\psi(t) \sqrt{\lambda p} \varphi \rho) o(t)+\pi_{3} \beta_{1} u(t)+\psi(t) \sqrt{\lambda p} \varphi \sqrt{1-\rho^{2}} w(t)\right) f^{\prime}(x) \\& +\frac{1}{2}\left((q(t) \sigma \sqrt{\lambda}+\psi(t) \sqrt{\lambda p} \varphi \rho)^{2}+\pi_{3}^{2} \beta_{1}^{2}+\psi(t)^{2} \lambda p \varphi^{2}\left(1-\rho^{2}\right)\right) f^{\prime \prime}(x),\end{aligned}$

可以发现, 当保险公司的初始财富为 $x\geq\frac{\mu\lambda(\theta_{2}-\theta_{1})}{r}$

定理 3.1 (验证定理) 若 $v_{2}(x)\in\mathcal{C}^{2}$ $v_{2}(a)=1$ $V_{2}(x)=v_{2}(x)$ .

定理 3.2 (证明见附录) 对于问题 (3.1), 取 $\phi(x)=x$ $V_2(x)$ $V_{2}(x)=e^{-K_2(x-a)},$

$\left\{\begin{aligned}o^{*}(t) & =-\frac{(q(t) \sqrt{\lambda} \sigma+\psi(t) \varphi \sqrt{\lambda p} \rho) K_{2}}{\eta_{1}}, \\u^{*}(t) & =-\frac{\pi_{3} \beta_{1} K_{2}}{\eta_{2}}, \\w^{*}(t) & =-\frac{\psi(t) \varphi \sqrt{\lambda p} \sqrt{1-\rho^{2}} K_{2}}{\eta_{3}},\end{aligned}\right.$

$\left\{\begin{array}{l}\pi_{3}^{*}=\frac{\left(\alpha_{1}-r\right) \eta_{2}}{\beta_{1}^{2}\left(1+\eta_{2}\right) K_{2}} \\q^{*}(t)=\frac{\mu \lambda \theta_{2} \eta_{1}}{\lambda \sigma^{2}\left(1+\eta_{1}\right) K_{2}}+\frac{\left(\mu \lambda \sqrt{p} \varphi \rho^{2} \theta_{2}+\lambda p \varphi \sigma \rho \theta_{3}\right) \eta_{3}}{\lambda \sqrt{p} \sigma^{2} \varphi\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{2}} \\\psi^{*}(t)=-\frac{\left(\mu \lambda \sqrt{p} \varphi \rho \theta_{2}+\lambda p \varphi \sigma \theta_{3}\right) \eta_{3}}{\lambda p \varphi^{2} \sigma\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{2}}\end{array}\right.$

注 3.1 在极端情况下, 当$\eta_{1} \rightarrow \infty$ $\eta_{2} \rightarrow\infty$ $\eta_{3} \rightarrow \infty$ $\mathbb{P}$

$\left\{\begin{array}{l}\pi_{3}^{*}=\frac{\alpha_{1}-r}{\beta_{1}^{2} K_{0}}, \\q^{*}(t)=\frac{\mu \theta_{2}+\sqrt{p} \sigma \rho \theta_{3}}{\sigma^{2}\left(1-\rho^{2}\right) K_{0}}, \\\psi^{*}(t)=-\frac{\mu \lambda \sqrt{p} \varphi \rho \theta_{2}+\lambda p \varphi \sigma \theta_{3}}{\lambda p \varphi^{2} \sigma\left(1-\rho^{2}\right) K_{0}}.\end{array}\right.$

值函数 $V_0(x)$ $V_0(x)=e^{-K_0(x-a)},$

同样地, 当 $\eta_{1} \rightarrow \infty$ $\eta_{2} \rightarrow \infty$

$\left\{\begin{array}{l}\pi_{3}^{*}=\frac{\alpha_{1}-r}{\beta_{1}^{2} K_{1}} \\q^{*}(t)=\frac{\mu \lambda \sqrt{p} \varphi\left(1-\rho^{2}\right) \theta_{2}+\left(\mu \lambda \sqrt{p} \varphi \theta_{2}+\lambda p \varphi \sigma \rho \theta_{3}\right) \eta_{3}}{\lambda \sqrt{p} \varphi \sigma^{2}\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{1}} \\\psi^{*}(t)=-\frac{\left(\mu \lambda \sqrt{p} \varphi \rho \theta_{2}+\lambda p \varphi \sigma \theta_{3}\right) \eta_{3}}{\lambda p \varphi^{2} \sigma\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{1}}\end{array}\right.$

值函数 $V_1(x)$ $V_1(x)=e^{-K_1(x-a)},$

4 数值分析

本节通过一些数值模拟来分析模型不确定下保险公司的最优投资-再保险-巨灾债券发行策略, 揭示关键因素对其的影响. 参考文献 [32 ,40 ,42 ], 本文参数取值见表 1 .

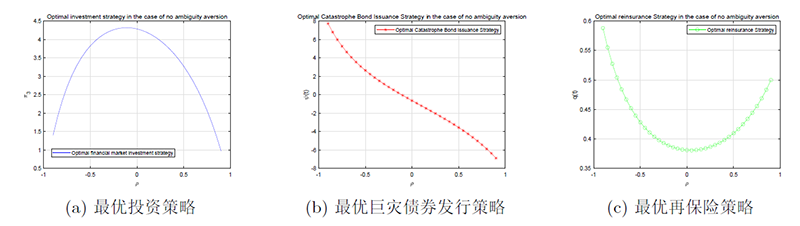

图 1 揭示了保险市场与巨灾债券市场之间相关系数 $\rho$ 的变动对保险公司最优投资-再保险- 巨灾发行策略产生的深远影响. 观察发现, 当相关系数 $\rho$ 在区间 $(-0.9, 0.9)$ 内逐步变化时, 保险公司在金融市场的最优投资策略 $\pi_{3}$ 呈现出先增后减的趋势, 这一转折发生在 $\rho$ 达到某一特定阈值之后. 同时, 保险公司巨灾债券的发行量 $\psi(t)$ 起初逐渐减少, 直至 $\rho$ 达到另一特定值, 此时保险公司停止发行巨灾债券, 并随着相关性的进一步增强, 转而开始购买巨灾债券. 保险公司的最优再保险策略, 其自留额 $q(t)$ 则先降后升, 意味着保险公司购买再保险的比例先升后降.

图1

图1

确定模型下 $\rho$ 对最优投资-再保险-巨灾债券发行策略的影响

由此可以看出: 巨灾债券成为了保险公司对冲风险的有效工具. 当巨灾债券和保险市场呈现负相关时, 保险公司倾向于发行巨灾债券, 以此筹集资金并转移部分潜在损失风险. 此时, 相较于传统的再保险方式, 发行巨灾债券更为灵活且成本较低效益更高, 因此保险公司减少再保险的购买. 然而, 当两市场呈现正相关, 保险公司发行巨灾债券的吸引力降低, 因为发行巨灾债券无法有效对冲保险市场的风险. 保险公司会选择购买巨灾债券, 以寻求额外的风险覆盖, 或在某些情况下, 通过持有这些债券来分散投资风险. 此时, 由于两市场的高度相关性, 保险公司会增加对金融市场的直接投资以追求更高回报, 同时适度调整再保险策略, 以平衡风险与收益. 当保险市场与巨灾债券市场的相关性极低时, 巨灾债券作为风险对冲工具的价值减弱. 在这种情况下, 保险公司更倾向于将资金投向金融市场以获取更高收益, 并增加再保险的购买量, 以更直接地管理其在保险市场面临的风险.

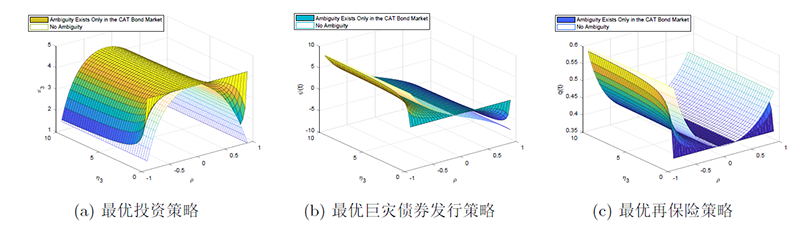

图 2 揭示了巨灾债券市场存在模型不确定时, 保险公司最优投资-再保险-巨灾发行策略的调整趋势. 当考虑巨灾债券市场的模型不确定时, 保险公司的行为反应显得尤为关键. 具体而言, 这种不确定性促使保险公司增加了对金融市场的投资力度. 这一变化反映出, 在巨灾债券市场预测难度加大的背景下, 保险公司倾向于将更多资源配置于模型相对更为确定、风险更为可控的金融市场, 以寻求更为稳定的收益.

图2

图2

模型不确定只存在于巨灾债券市场与确定模型下相关策略的对比

同时, 对于巨灾债券的发行与购买, 模型不确定性带来了显著的负向影响. 由于巨灾风险模型的准确性直接关系到巨灾债券的定价与风险评估, 模型的不确定性使得保险公司难以精确估算, 进而影响了债券的合理定价. 因此, 为了规避这一不确定性带来的潜在风险, 保险公司选择谨慎行事, 减少巨灾债券的发行量和购买数量, 以降低因模型不准确而可能引发的损失.

此外, 保险市场与巨灾债券市场之间的相关性也使得模型不确定性对保险公司的再保险策略产生了影响. 在面临模型不确定性的情况下, 保险公司为了更有效地管理风险, 倾向于增加购买再保险的比例. 再保险作为一种风险转移机制, 能够帮助保险公司分散和减轻灾难事件带来的财务压力. 因此, 在模型不确定性增加的背景下, 保险公司更倾向于通过购买再保险来增强自身的风险抵御能力, 而非依赖可能存在定价偏差的巨灾债券.

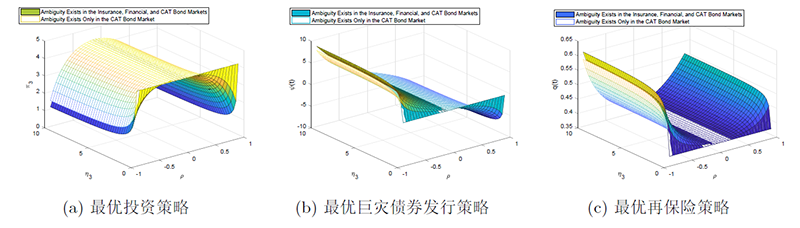

图 3 ($\eta_{1}=2$, $\eta_{2}=2$), 探讨保险、金融及巨灾债券市场均存在模型不确定时, 保险公司的最优投资与再保险策略如何调整. 图示清晰展示了, 当金融市场存在模型不确定时, 保险公司会倾向于减少在该市场上对风险资产的投资. 进一步分析发现, 即便保险与巨灾债券市场同样存在模型不确定, 与仅巨灾债券市场面临不确定的情形相比, 保险公司会减少再保险的购买. 此外, 保险市场与巨灾债券市场之间的相关性对保险公司的巨灾债券策略具有显著影响; 两者负相关时, 保险公司倾向于增加巨灾债券的发行; 正相关时, 则更倾向于购买巨灾债券.

图3

图3

模型不确定只存在于巨灾债券市场与三市场均存在模型不确定下相关策略的对比

这一策略调整背后的经济学逻辑在于: 保险市场与巨灾债券市场的负相关关系意味着两者在灾难事件中的表现往往呈现对冲效应. 在此情境下, 购买再保险可能被视为一种成本较高的风险管理手段, 因为再保险费用可能随保险市场的波动而变动, 相比之下, 巨灾债券的融资成本则相对稳定. 因此, 保险公司可能更倾向于利用巨灾债券来构建更为稳健的成本结构, 以降低对再保险的依赖. 而当保险市场与巨灾债券市场正相关时, 购买巨灾债券成为保险公司多元化风险敞口的有效途径. 通过持有巨灾债券, 保险公司不仅能够在传统保险合同之外实现风险分散, 还能有效降低对单一灾难风险的暴露程度, 即便金融市场模型的不确定性可能对这两个市场产生联动影响, 保险公司通过持有巨灾债券也能实现风险分布的多样化, 增强整体风险抵御能力.

图 4 ($\rho=-0.7$, $\eta_{1}=2$,$\eta_{2}=2$) 中, 我们展示了模型不确定性条件下资金对最优投资-再保险策略的影响, 从图中分析可得, 保险公司的目标函数为最小化破产概率, 其风险偏好随资产的增加而趋于保守. 具体表现为, 随着资金的增长, 保险公司会减少在金融市场风险资产上的投资, 同时减少巨灾债券的发行, 并增加再保险的购买量. 当保险公司的资金达到或超过某一特定阈值, 即 $x\geq\frac{\mu\lambda(\theta_{2}-\theta_{1})}{r}$ 时, 其策略发生显著变化. 此时, 保险公司选择将全部资金投资于金融市场的无风险资产以获取稳定的无风险利息收入, 而部分索赔风险则通过再保险机制转移给再保险公司, 其转移成本完全由无风险利息收入来覆盖. 在这种情境下, 保险公司不再投资于有风险的市场资产 (即 $\pi_{3}=0$), 停止发行巨灾债券 (即 $\psi(t)=0$), 并且将所有索赔风险通过再保险转嫁 (即 $q(t)=0$).

图4

图4

模型不确定下保险公司的资金 $x$ 对相关策略的影响

进一步观察可以发现, 随着巨灾债券市场模糊厌恶系数的增大, 保险公司的行为也发生调整. 具体来说, 保险公司会增加巨灾债券的发行量, 同时减少在金融市场风险资产上的投资以及再保险的购买比例. 保险公司作为风险规避者, 在面临市场不确定性时更倾向于采取保守策略以确保财务稳定. 当巨灾债券市场的模糊厌恶系数上升时 (巨灾债券市场的模糊性减弱), 这实际上反映了保险公司对该市场模型信心的增强, 因此它们更愿意利用这一市场, 通过发行巨灾债券来转移风险, 同时相应减少在其他风险资产上的暴露和再保险的依赖. 这种策略调整是保险公司在风险规避与寻求收益之间寻求平衡的结果.

5 结论

近年来, 气候和环境变化加剧了全球自然灾害的频发, 这对社会稳定和全球经济构成了严峻挑战, 同时也使保险公司面临着巨大的巨灾风险损失. 因此, 巨灾债券的发行成为提升保险公司避免巨大损失的新途径. 保险公司可以通过转变传统经营模式, 通过巨灾风险证券化将部分风险转移至资本市场上, 利用其强大的风险容纳能力和资金配置能力, 实现风险的分散.

在传统保险市场中, 风险资产主要通过投资组合收益间接覆盖保险损失, 其对冲效果和金融与保险市场的相关性紧密关联, 需依赖市场有效性实现风险分散. 相比之下, 巨灾债券能直接将保险风险转移至资本市场, 其赔付与灾害事件直接挂钩, 但可能因依赖外生触发指标而与实际损失产生偏差. 保险公司在发行 (购买) 巨灾债券时, 其购买再保险的比例会随发行 (购买) 数量的增加而减少, 由此可见巨灾债券可以作为保险公司对冲风险的良好金融工具. 同时, 巨灾债券市场与保险市场的相关性对保险公司的投资组合以及风险管理策略也会产生显著的影响, 相关性越强 ($\mid\rho\mid$ 越大) 保险公司对风险资产的投资就越少, 发行 (购买) 巨灾债券的越多, 购买再保险就越少. 在保险、金融、巨灾债券三个市场都存在模型不确定性的情况下, 保险公司可能更倾向于依赖巨灾债券, 以实现更稳定的成本结构和更有效的风险分散. 通过对不同市场的模糊厌恶系数进行对比分析可以发现, 由于保险公司具有强烈的风险规避倾向, 它们更倾向于将资金投资模型更为确定的市场. 同时, 最优投资策略是资金 $x$ 的递减函数, 保险公司拥有的财富越多, 其投资意愿越低, 而购买再保险的倾向则越强.

附录 (定理 3.2 的证明)

证

(A.1) $\begin{array}{l}\inf _{\pi \in \mathbb{V}} \sup _{o, u, w}\left[\left(x r+\pi_{3}\left(\alpha_{1}-r\right)+\mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\lambda p \varphi \theta_{3} \psi(t)\right.\right. \\\left.+(q(t) \sigma \sqrt{\lambda}+\sqrt{\lambda p} \varphi \rho \psi(t)) o(t)+\pi_{3} \beta_{1} u(t)+\sqrt{\lambda p} \varphi \sqrt{1-\rho^{2}} \psi(t) w(t)\right) V_{2}^{\prime}(x) \\+\frac{1}{2}\left((q(t) \sigma \sqrt{\lambda}+\sqrt{\lambda p} \varphi \rho \psi(t))^{2}+\pi_{3}^{2} \beta_{1}^{2}+\lambda p \varphi^{2}\left(1-\rho^{2}\right) \psi(t)^{2}\right) V_{2}^{\prime \prime}(x) \\\left.-\frac{1}{2} \eta_{1} \phi\left(V_{2}(x)\right)[o(t)]^{2}-\frac{1}{2} \eta_{2} \phi\left(V_{2}(x)\right)[u(t)]^{2}-\frac{1}{2} \eta_{3} \phi\left(V_{2}(x)\right)[w(t)]^{2}\right]=0.\end{array}$

(A.2) $\left\{\begin{array}{l}o^{*}(t)=\frac{(q(t) \sqrt{\lambda} \sigma+\psi(t) \varphi \sqrt{\lambda p} \rho) V_{2}^{\prime}(x)}{\xi_{1} V_{2}(x)}, \\u^{*}(t)=\frac{\pi_{3} \beta_{1} V_{2}^{\prime}(x)}{\xi_{2} V_{2}(x)}, \\w^{*}(t)=\frac{\psi(t) \varphi \sqrt{\lambda p} \sqrt{1-\rho^{2}} V_{2}^{\prime}(x)}{\xi_{3} V_{2}(x)}.\end{array}\right.$

(A.3) $\begin{aligned}\inf _{\pi \in \mathbb{V}} & {\left[\left(x r+\pi_{3}\left(\alpha_{1}-r\right)+\mu \lambda\left[\theta_{1}-\theta_{2}(1-q(t))\right]-\lambda p \varphi \theta_{3} \psi(t)+\frac{(q(t) \sqrt{\lambda} \sigma+\psi(t) \varphi \sqrt{\lambda p} \rho)^{2} V_{2}^{\prime}(x)}{2 \eta_{1} V_{2}(x)}\right.\right.} \\& \left.+\frac{\pi_{3}^{2} \beta_{1}^{2} V_{2}^{\prime}(x)}{2 \eta_{2} V_{2}^{\prime}(x)}+\frac{\psi(t)^{2} \lambda p \varphi^{2}\left(1-\rho^{2}\right) V_{2}^{\prime}(x)}{2 \eta_{3} V_{2}^{\prime}(x)}\right) V_{2}^{\prime}(x)+\frac{1}{2}\left((q(t) \sigma \sqrt{\lambda}+\sqrt{\lambda p} \varphi \rho \psi(t))^{2}\right. \\& \left.\left.+\pi_{3}^{2} \beta_{1}^{2}+\lambda p \varphi^{2}\left(1-\rho^{2}\right) \psi(t)^{2}\right) V_{2}^{\prime \prime}(x)\right]=0\end{aligned}$

参考 Liu (2024) 对值函数的求解可知, Hamilton-Jacobi-Bellman (HJB) 方程 (A.3) 的解满足 $V_{2}'(x) > 0$ $V_{2}''(x) < 0$ $\pi_{3}$ $q(t)$ $\psi(t)$

(A.4) $\left\{\begin{array}{l}\pi_{3}^{*}=-\frac{\left(\alpha_{1}-r\right) \eta_{2} V_{2}(x) V_{2}^{\prime}(x)}{\beta_{1}^{2}\left(V_{2}^{\prime}(x)^{2}+\eta_{2} V_{2}(x) V_{2}^{\prime \prime}(x)\right)}, \\q^{*}(t)=-\frac{\mu \lambda \theta_{2} \eta_{1} V_{2}(x) V_{2}^{\prime}(x)}{\lambda \sigma^{2}\left(V_{2}^{\prime}(x)^{2}+\eta_{1} V_{2}(x) V_{2}^{\prime \prime}(x)\right)}-\frac{\left(\mu \lambda \sqrt{p} \varphi \rho^{2} \theta_{2}+\lambda p \varphi \sigma \rho \theta_{3}\right) \eta_{3} V_{2}(x) V_{2}^{\prime}(x)}{\lambda \sqrt{p} \sigma^{2} \varphi\left(1-\rho^{2}\right)\left(V_{2}^{\prime}(x)^{2}+\eta_{3} V_{2}(x) V_{2}^{\prime \prime}(x)\right)}, \\\psi^{*}(t)=\frac{\left(\mu \lambda \sqrt{p} \varphi \rho \theta_{2}+\lambda p \varphi \sigma \theta_{3}\right) \eta_{3} V_{2}(x) V_{2}^{\prime}(x)}{\lambda p \varphi^{2} \sigma\left(1-\rho^{2}\right)\left(V_{2}^{\prime}(x)^{2}+\eta_{3} V_{2}(x) V_{2}^{\prime \prime}(x)\right)}.\end{array}\right.$

将 (A.4) 式代入 HJB 公式 (A.3) 并化简, 我们有

(A.5) $\begin{matrix}\label{25} \nonumber &xrV_{2}'(x)-\dfrac{(\alpha_{1}-r)^{2}\eta_{2}V_{2}(x)V_{2}'(x)^{2}}{\beta_{1}^{2}(V_{2}'(x)^{2}+\eta_{2}V_{2}(x)V_{2}''(x))} +\mu\lambda(\theta_{1}-\theta_{2})V_{2}(x)-\dfrac{\mu^{2}\lambda\theta_{2}^{2}\eta_{1}V_{2}(x)V_{2}'(x)^{2}} {\sigma^{2}(V_{2}'(x)^{2}+\eta_{1}V_{2}(x)V_{2}''(x))}\\ \nonumber&-\dfrac{\mu^{2}\lambda\theta_{2}^{2}\rho^{2}\eta_{3}V_{2}(x)V_{2}'(x)^{2}}{\sigma^{2}(1-\rho^{2})(V_{2}'(x)^{2} +\eta_{3}V_{2}(x)V_{2}''(x))}-\dfrac{2\mu\lambda\sqrt{p}\rho\theta_{2}\theta_{3} \eta_{3}V_{2}(x)V_{2}'(x)^{2}}{\sigma(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))}\\ \nonumber&-\dfrac{\lambda p\theta_{3}^{2}\eta_{3}V_{2}(x)V_{2}'(x)^{2}}{(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))} +\dfrac{\mu^{2}\lambda\theta_{2}^{2}\eta_{1}V_{2}(x)V_{2}'(x)^{4}}{2\sigma^{2}(V_{2}'(x)^{2}+\eta_{1} V_{2}(x)V_{2}''(x))^{2}}\\ \nonumber&+\dfrac{(\alpha_{1}-r)^{2}\eta_{2}V_{2}(x)V_{2}'(x)^{4}}{2\beta_{1}^{2}(V_{2}'(x)^{2} +\eta_{2}V_{2}(x)V_{2}''(x))^{2}}+\dfrac{\mu^{2}\lambda\theta_{2}^{2}\rho^{2}\eta_{3}V_{2}(x)V_{2}'(x)^{4}} {2\sigma^{2}(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))^{2}}\\ \nonumber&+\dfrac{\mu\lambda\sqrt{p}\rho\theta_{2}\theta_{3}\eta_{3}V_{2}(x)V_{2}'(x)^{4}}{\sigma(1-\rho^{2})(V_{2}'(x)^{2} +\eta_{3}V_{2}(x)V_{2}''(x))^{2}}+\dfrac{\lambda p\theta_{3}^{2}\eta_{3}V_{2}(x)V_{2}'(x)^{4}}{2(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))^{2}}\\ \nonumber&+\dfrac{\mu^{2}\lambda\theta_{2}^{2}\eta_{1}^{2}V_{2}(x)^{2}V_{2}'(x)^{2}V_{2}''(x)}{2\sigma^{2}(V_{2}'(x)^{2} +\eta_{1}V_{2}(x)V_{2}''(x))^{2}}+\dfrac{\mu^{2}\lambda\theta_{2}^{2}\rho^{2}\eta_{3}^{2} V_{2}(x)^{2}V_{2}'(x)^{2}V_{2}''(x)}{2\sigma^{2}(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))^{2}}\\ \nonumber&+\dfrac{\mu\lambda\sqrt{p}\rho\theta_{2}\theta_{3}\eta_{3}^{2}V_{2}(x)^{2}V_{2}'(x)^{2}V_{2}''(x)} {\sigma(1-\rho^{2})(V_{2}'(x)^{2}+\eta_{3}V_{2}(x)V_{2}''(x))^{2}}+\dfrac{\lambda p\theta_{3}^{2}\eta_{3}^{2}V_{2}(x)^{2}V_{2}'(x)^{2}V_{2}''(x)}{2(1-\rho^{2})(V_{2}'(x)^{2} +\eta_{3}V_{2}(x)V_{2}''(x))^{2}}\\ &+\dfrac{(\alpha_{1}-r)^{2}\eta_{2}^{2}V_{2}(x)^{2}V_{2}'(x)^{2}V_{2}''(x)} {2\beta_{1}^{2}(V_{2}'(x)^{2}+\eta_{2}V_{2}(x)V_{2}''(x))^{2}}=0. \end{matrix}$

由上述式子以及边界条件等, 推测值函数的具体形式为

进一步, 我们有$V_{2}'(x)=-K_{2}V_2(x),\hspace{1em} V_{2}''(x)=K_{2}^{2}V_2(x).$ $V_{2}(x)$ $V_{2}'(x)$ $V_{2}''(x)$

根据边界条件 $V_{2}(a)=1$ $L_{2}=1$ . 因此,

所以, 我们得到保险公司的最优投资-再保险-巨灾债券发行策略如下

$\left\{\begin{array}{l}\pi_{3}^{*}=\frac{\left(\alpha_{1}-r\right) \eta_{2}}{\beta_{1}^{2}\left(1+\eta_{2}\right) K_{2}}, \\q^{*}(t)=\frac{\mu \lambda \theta_{2} \eta_{1}}{\lambda \sigma^{2}\left(1+\eta_{1}\right) K_{2}}+\frac{\left(\mu \lambda \sqrt{p} \varphi \rho^{2} \theta_{2}+\lambda p \varphi \sigma \rho \theta_{3}\right) \eta_{3}}{\lambda \sqrt{p} \sigma^{2} \varphi\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{2}}, \\\psi^{*}(t)=-\frac{\left(\mu \lambda \sqrt{p} \varphi \rho \theta_{2}+\lambda p \varphi \sigma \theta_{3}\right) \eta_{3}}{\lambda p \varphi^{2} \sigma\left(1-\rho^{2}\right)\left(1+\eta_{3}\right) K_{2}}.\end{array}\right.$

参考文献

View Option

[1]

Browne S Optimal investment policies for a firm with a random risk process: exponential utility and minimizing the probability of ruin

Mathematics of Operations Research , 1995 , 20 4 ): 937 -958

DOI:10.1287/moor.20.4.937

URL

[本文引用: 1]

We consider a firm that is faced with an uncontrollable stochastic cash flow, or random risk process. There is one investment opportunity, a risky stock, and we study the optimal investment decision for such firms. There is a fundamental incompleteness in the market, in that the risk to the investor of going bankrupt cannot be eliminated under any investment strategy, since the random risk process ensures that there is always a positive probability of ruin (bankruptcy). We therefore focus on obtaining investment strategies which are optimal in the sense of minimizing the risk of ruin. In particular, we solve for the strategy that maximizes the probability of achieving a given upper wealth level before hitting a given lower level. This policy also minimizes the probability of ruin. We prove that when there is no risk-free interest rate, this policy is equivalent to the policy that maximizes utility from terminal wealth, for a fixed terminal time, when the firm has an exponential utility function. This validates a longstanding conjecture about the relation between minimizing probability of ruin and exponential utility. When there is a positive risk-free interest rate, the conjecture is shown to be false. We also solve for the optimal policy for the related objective of minimizing the expected discounted penalty paid upon ruin.

[3]

Promislow S D Young V R Minimizing the probability of ruin when claims follow Brownian motion with drift

North American Actuarial Journal , 2005 , 9 3 ): 109 -128

DOI:10.1080/10920277.2005.10596229

URL

[本文引用: 1]

[5]

Lin X Li Y F Optimal reinsurance and investment for a jump diffusion risk process under the CEV model

North American Actuarial Journal , 2011 , 15 3 ): 417 -431

DOI:10.1080/10920277.2011.10597628

URL

[本文引用: 1]

[6]

Li D Zeng Y Yang H Robust optimal excess-of-loss reinsurance and investment strategy for an insurer in a model with jumps

Scandinavian Actuarial Journal , 2018 , 2018 2 ): 145 -171

DOI:10.1080/03461238.2017.1309679

URL

[本文引用: 1]

[7]

Bai L Guo J Optimal proportional reinsurance and investment with multiple risky assets and no-shorting constraint

Insurance: Mathematics and Economics , 2008 , 42 3 ): 968 -975

DOI:10.1016/j.insmatheco.2007.11.002

URL

[本文引用: 1]

[8]

Jin Z Xu Z Q Zou B A perturbation approach to optimal investment, liability ratio, and dividend strategies

Scandinavian Actuarial Journal , 2022 , 2022 2 ): 165 -188

DOI:10.1080/03461238.2021.1938199

URL

[本文引用: 1]

[9]

张帅琪 , 刘国欣 . 复合 Poisson 模型带比例与固定交易费用的最优分红与注资

中国科学: 数学 , 2012 , 42 8 ): 827 -843

[本文引用: 1]

Zhang S Q Liu G X Optimal dividend payment and capital injection of the compound Poisson risk model with both proportional and fixed costs Sci Sin Math

2012 , 42 8 ): 827 -843 (in Chinese).

[本文引用: 1]

[10]

Yao D Wang R Xu L Optimal dividend and capital injection strategy with fixed costs and restricted dividend rate for a dual model

Journal of Industrial and Management Optimization , 2014 , 10 4 ): 1235 -1259

DOI:10.3934/jimo.2014.10.1235

URL

[11]

Zhou M Yuen K C Portfolio selection by minimizing the present value of capital injection costs

ASTIN Bulletin , 2015 , 45 1 ): 207 -238

DOI:10.1017/asb.2014.22

URL

This paper considers the portfolio selection and capital injection problem for a diffusion risk model within the classical Black–Scholes financial market. It is assumed that the original surplus process of an insurance portfolio is described by a drifted Brownian motion, and that the surplus can be invested in a risky asset and a risk-free asset. When the surplus hits zero, the company can inject capital to keep the surplus positive. In addition, it is assumed that both fixed and proportional costs are incurred upon each capital injection. Our objective is to minimize the expected value of the discounted capital injection costs by controlling the investment policy and the capital injection policy. We first prove the continuity of the value function and a verification theorem for the corresponding Hamilton–Jacobi–Bellman (HJB) equation. We then show that the optimal investment policy is a solution to a terminal value problem of an ordinary differential equation. In particular, explicit solutions are derived in some special cases and a series solution is obtained for the general case. Also, we propose a numerical method to solve the optimal investment and capital injection policies. Finally, a numerical study is carried out to illustrate the effect of the model parameters on the optimal policies.

[12]

李鹏 , 周明 , 孟辉 . 脉冲和正则控制下的最优注资: 一种混合策略

中国科学: 数学 , 2018 , 48 4 ): 565 -578

Li P Zhou M Meng H Optimal stochastic impulse and regular control for capital injections: A hybrid strategy Sci Sin Math , 2018 , 48 4 ): 565 -578 (in Chinese).

[13]

陈树敏 , 曾燕 , 谷爱玲 . R $\& $

系统工程理论与实践 , 2019 , 39 6 ): 1394 -1406

DOI:10.12011/1000-6788-2018-0276-13

本文研究了存在新技术项目时R&D企业的最优技术投资与分红策略.假定企业流动资金变化由对偶风险模型描述,企业破产时存在清算价值,目标是最大化破产前的累计红利现值与清算价值现值之和.运用混合奇异控制-最优停时方法,当企业的每笔收益服从指数分布时本文得到R&D企业的最优投资与分红策略及最优值函数的解析表达式.最后,我们分析了模型参数对企业最优投资与分红策略的影响,并用效用无偏差理论分析了新技术项目的价值.

Chen M Zeng Y Gu A L Optimal technology investment-dividend strategy for a R$\&$

Systems Engineering-Theory $\&$ , 2019 , 39 6 ): 1394 -1406

[14]

Guan C Xu Z Q Zhou R Dynamic optimal reinsurance and dividend payout in finite time horizon

Mathematics of Operations Research , 2023 , 48 1 ): 544 -568

DOI:10.1287/moor.2022.1276

URL

[本文引用: 1]

[15]

姚海祥 , 伍慧玲 , 曾燕 . 不确定终止时间和通货膨胀影响下风险资产的最优投资策略

系统工程理论与实践 , 2014 , 34 5 ): 1089 -1099

DOI:10.12011/1000-6788(2014)5-1089

[本文引用: 1]

本文基于连续时间均值-方差框架,研究了通货膨胀影响下投资终止时间不确定的最优投资组合选择问题. 与以往大多数文献不同,本文所考虑的金融市场仅存在风险资产. 首先构建了含通货膨胀及终止时间不确定因素的风险资产均值-方差投资组合选择模型. 然后利用随机动态规划方法和Lagrange对偶原理得到了有效投资策略及有效边界的解析表达式,并进一步讨论了本文模型的几种特殊情形. 最后,通过数值算例对本文所得结论进行阐述.

Yao H X Wu H L Zeng Y Optimal investment strategy for risky assets under uncertain time-horizon and inflation

Systems Engineering-Theory $\&$ , 2014 , 34 5 ): 1089 -1099

[本文引用: 1]

[16]

Guan G Liang Z Optimal reinsurance and investment strategies for insurer under interest rate and inflation risks

Insurance: Mathematics and Economics , 2014 , 55 105 -115

DOI:10.1016/j.insmatheco.2014.01.007

URL

[17]

伍慧玲 , 董洪斌 . 带有通货膨胀风险和随机收入的确定缴费养老金计划

系统工程理论与实践 , 2016 , 36 3 ): 545 -558

DOI:10.12011/1000-6788(2016)03-0545-14

在离散时间框架下研究了一个多期均值-方差确定缴费养老基金管理问题. 综合考虑了金融资产价格、通货膨胀和随机收入这三种决策风险, 且假设养老计划参与者的随机收入会受到通货膨胀的影响. 分析了最优策略的存在性, 运用拉格朗日对偶原理和动态规划方法, 得到了最优投资策略和有效前沿的显式解. 最后运用数值分析方法, 分析了通货膨胀和随机收入对投资策略、终端真实财富均值和有效前沿的影响. 我们的研究表明, 通货膨胀和随机收入会对相关结果产生本质的影响.

Wu H L Dong H B Multi-period mean-variance defined contribution pension management with inflation and stochastic income

Systems Engineering-Theory $\&$ , 2016 , 36 3 ): 545 -558

[18]

曾燕 , 黄金波 . 基于均值-AS 模型的资产配置

管理科学学报 , 2016 , 19 2 ): 95 -108

[本文引用: 1]

Zeng Y Huang J B Asset allocation based on mean-AS model

Journal of Management Science in China , 2016 , 19 2 ): 95 -108

[本文引用: 1]

[19]

Yao H X Li Z F Li D Multi-period mean-variance portfolio selection with stochastic interest rate and uncontrollable liability

European Journal of Operational Research , 2016 , 252 3 ): 837 -851

DOI:10.1016/j.ejor.2016.01.049

URL

[本文引用: 1]

[20]

Yang Y Wang G J Yao J Time-consistent reinsurance-investment games for multiple mean-variance insurers with mispricing and default risks

Insurance: Mathematics and Economics , 2024 , 114 79 -107

DOI:10.1016/j.insmatheco.2023.11.004

URL

[本文引用: 1]

[21]

Liang Z Yuen K C Optimal dynamic reinsurance with dependent risks: variance premium principle

Scandinavian Actuarial Journal , 2016 , 2016 1 ): 18 -36

DOI:10.1080/03461238.2014.892899

URL

[本文引用: 2]

[22]

Wang W Y Zhang Z M Computing the Gerber-Shiu function by frame duality projection. Scandinavian Actuarial Journal , 2019 , 2019 4 ): 291 -307

[23]

Yuan Y Han X Liang Z Yuen K C Optimal reinsurance-investment strategy with thinning dependence and delay factors under mean-variance framework

European Journal of Operational Research , 2023 , 311 2 ): 581 -595

DOI:10.1016/j.ejor.2023.05.023

URL

[24]

Rong X Yan Y Zhao H Optimal reinsurance and investment problem with multiple risky assets and correlation risk for an insurer under the Ornstein-Uhlenbeck model

Communications in Statistics-Theory and Methods , 2024 , 53 8 ): 2689 -2714

DOI:10.1080/03610926.2022.2148470

URL

[本文引用: 1]

[25]

Shen Y Zeng Y Optimal investment-reinsurance strategy for mean-variance insurers with square-root factor process

Insurance: Mathematics and Economics , 2015 , 62 3 ): 118 -137

DOI:10.1016/j.insmatheco.2015.03.009

URL

[本文引用: 1]

[26]

Liu B Meng H Zhou M Optimal investment and reinsurance policies for an insurer with ambiguity aversion

North American Journal of Economics and Finance , 2021 , 55 : Art 101303

[27]

Dong X Rong X M Zhao H Non-zero-sum reinsurance and investment game with non-trivial curved strategy structure under Ornstein-Uhlenbeck process

Scandinavian Actuarial Journal , 2023 , 2023 6 ): 565 -597

DOI:10.1080/03461238.2022.2139631

URL

[本文引用: 1]

[28]

Anderson E Hansen L P Sargent T A quartet of semigroups for model specification, robustness, prices of risk, and model detection

Journal of the European Economic Association , 2003 , 1 1 ): 68 -123

DOI:10.1162/154247603322256774

URL

[本文引用: 1]

[29]

Yi B Li Z Viens F G Zeng Y Robust optimal control for an insurer with reinsurance and investment under heston's stochastic volatility model

Insurance Mathematics and Economics , 2013 , 53 3 ): 601 -614

DOI:10.1016/j.insmatheco.2013.08.011

URL

[本文引用: 1]

[30]

Hu D Chen S Wang H Robust reinsurance contracts with uncertainty about jump risk

European Journal of Operational Research , 2018 , 266 3 ): 1175 -1188

DOI:10.1016/j.ejor.2017.10.061

URL

[本文引用: 1]

[31]

Bayraktar E Zhang Y Minimizing the probability of lifetime ruin under ambiguity aversion

SIAM Journal on Control and Optimization , 2015 , 53 1 ): 58 -90

DOI:10.1137/140955999

URL

[本文引用: 1]

[32]

Sun Z Zheng X Zhang X Robust optimal investment and reinsurance of an insurer under variance premium principle and default risk

Journal of Mathematical Analysis and Applications , 2017 , 446 2 ): 1666 -1686

DOI:10.1016/j.jmaa.2016.09.053

URL

[本文引用: 2]

[33]

李仲飞 , 袁子甲 . 参数不确定性下资产配置的动态均值-方差模型 . 管理科学学报 , 2010 , 13 12 ): 1 -9

[本文引用: 1]

Li Z F Yuan Z J A dynamic mean-variance model of portfolio selection under parameter uncertainty

Journal of management science in China , 2010 , 13 12 ): 1 -9

[本文引用: 1]

[34]

宫晓琳 , 杨淑振 , 胡金焱 , 张宁 . 非线性期望理论与基于模型不确定性的风险度量

经济研究 , 2015 , 578 11 ): 135 -149

Gong X L Yang S Z Hu J Y Zhang N Non-linear expectation theory and risk measurement based on model ambiguity

Economic Research Journal , 2015 , 578 11 ): 135 -149

[35]

Zeng Y Li D Gu A Robust equilibrium reinsurance-investment strategy for a mean-variance insurer in a model with jumps

Insurance Mathematics and Economics , 2016 , 66 138 -152

DOI:10.1016/j.insmatheco.2015.10.012

URL

[36]

Zheng X X Zhou J M Sun Z Y Robust optimal portfolio and proportional reinsurance for an insurer under a CEV model

Insurance: Mathematics and Economics , 2016 , 67 77 -87

DOI:10.1016/j.insmatheco.2015.12.008

URL

[37]

刘兵 , 周明 . 模糊厌恶下的最优投资与最优保费策

系统工程理论与实践 , 2020 , 40 7 ): 1707 -1720

DOI:10.12011/1000-6788-2019-0365-14

保险公司的投资决策与保费收取决策至关重要.由于金融市场复杂性与风险性等特点,保险公司对金融市场的模型估计不可避免的会存在模糊性.因此在金融市场存在模糊性下研究保险公司的最优投资和最优保费策略会更加贴近现实.假设保险公司对金融市场的模型估计会存在模糊性,而保险公司对自己的模型由于其长时间的应用、经营和检验将不会存在模糊性.在模糊厌恶下,在最大化保险公司终端财富期望效用的目标下,给出了保险公司的最优投资和保费策略的解析解并得到了值函数具体的形式.结果显示:对金融市场模糊厌恶下求得的最优策略与不考虑模糊性下所求得的最优策略会存在联系,且金融市场的模糊性会对最优策略有明显的影响.

Liu B Zhou M Optimal investment and premium policies with ambiguity aversion

Systems Engineering-Theory $\&$ , 2020 , 40 7 ): 1707 -1720

[38]

孟辉 , 魏丽 , 周明 . 模糊厌恶下保险人的鲁棒再保险策略

中国科学: 数学 , 2021 , 51 11 ): 1791 -1818

Meng H Wei L Zhou M Robust reinsurance strategy under ambiguity-averse Sci Sin Math , 2021 , 51 11 ): 1791 -1818 (in Chinese).

[39]

王佩 , 李仲飞 , 张玲 . 不完全信息和模糊厌恶下 DC 型养老金最优投资策略

运筹与管理 , 2022 , 31 6 ): 125 -132

DOI:10.12005/orms.2022.0192

在信息部分可观测的金融市场中,参与者可投资于一个无风险资产、一个滚动债券和一支股票。其中,股票的预期收益率由一个服从均值-回复过程的预测因子预测。参与者是模糊厌恶的,只能观测到股票价格和利率,却无法观测到预测因子。利用滤波技术和动态规划原理,得到了不完全信息和模糊厌恶下DC型养老金最优投资策略的解析式。进一步,利用敏感性分析和比较静态分析,对比仅考虑不完全信息、仅考虑模糊厌恶以及同时考虑不完全信息和模糊厌恶三种情形下的最优投资策略。结果表明同时考虑不完全信息和模糊厌恶时的最优投资策略最保守,仅考虑不完全信息时的最优投资策略对风险厌恶系数的变化最敏感。

Wang P Li Z F Zhang L Optimal investment strategy for a DC pension with incomplete information and ambiguity aversion

Operations Research and Mangement Science , 2022 , 31 6 ): 125 -132

[40]

Liu B Zhang L Zhou M Portfolio selections for insurers with ambiguity aversion: minimizing the probability of ruin

Applied Economics , 2024 , 56 12 ): 1423 -1439

DOI:10.1080/00036846.2023.2176453

URL

[本文引用: 3]

[41]

Nell M Richter A Improving risk allocation through cat bonds

The Geneva Papers on Risk and Insurance , 2004 , 29 183 -201

[本文引用: 1]

[44]

Fleming W H Soner M Controlled Markov Processes and Viscosity Solutions . New York : Springer , 2006

[本文引用: 1]

Optimal investment policies for a firm with a random risk process: exponential utility and minimizing the probability of ruin

1

1995

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal proportional reinsurance policies in a dynamic setting

1

2001

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Minimizing the probability of ruin when claims follow Brownian motion with drift

1

2005

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal investment for insurer with jump-diffusion risk process

1

2005

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal reinsurance and investment for a jump diffusion risk process under the CEV model

1

2011

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Robust optimal excess-of-loss reinsurance and investment strategy for an insurer in a model with jumps

1

2018

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal proportional reinsurance and investment with multiple risky assets and no-shorting constraint

1

2008

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

A perturbation approach to optimal investment, liability ratio, and dividend strategies

1

2022

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

复合 Poisson 模型带比例与固定交易费用的最优分红与注资

1

2012

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal dividend payment and capital injection of the compound Poisson risk model with both proportional and fixed costs Sci Sin Math

1

2012

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal dividend and capital injection strategy with fixed costs and restricted dividend rate for a dual model

0

2014

Portfolio selection by minimizing the present value of capital injection costs

0

2015

脉冲和正则控制下的最优注资: 一种混合策略

0

2018

R $\& $ D 企业最优技术投资与分红策略研究

0

2019

Optimal technology investment-dividend strategy for a R$\&$ D firm

0

2019

Dynamic optimal reinsurance and dividend payout in finite time horizon

1

2023

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

不确定终止时间和通货膨胀影响下风险资产的最优投资策略

1

2014

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal investment strategy for risky assets under uncertain time-horizon and inflation

1

2014

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal reinsurance and investment strategies for insurer under interest rate and inflation risks

0

2014

带有通货膨胀风险和随机收入的确定缴费养老金计划

0

2016

Multi-period mean-variance defined contribution pension management with inflation and stochastic income

0

2016

基于均值-AS 模型的资产配置

1

2016

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Asset allocation based on mean-AS model

1

2016

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Multi-period mean-variance portfolio selection with stochastic interest rate and uncontrollable liability

1

2016

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Time-consistent reinsurance-investment games for multiple mean-variance insurers with mispricing and default risks

1

2024

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal dynamic reinsurance with dependent risks: variance premium principle

2

2016

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

... ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal reinsurance-investment strategy with thinning dependence and delay factors under mean-variance framework

0

2023

Optimal reinsurance and investment problem with multiple risky assets and correlation risk for an insurer under the Ornstein-Uhlenbeck model

1

2024

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal investment-reinsurance strategy for mean-variance insurers with square-root factor process

1

2015

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

Optimal investment and reinsurance policies for an insurer with ambiguity aversion

0

2021

Non-zero-sum reinsurance and investment game with non-trivial curved strategy structure under Ornstein-Uhlenbeck process

1

2023

... 事实上, 众多学者对保险公司投资与风险管理策略进行了广泛而深入的研究. Browne[1 ] 在最大化保险公司终端财富的期望效用以及最小化保险公司的破产概率目标下研究了保险公司的最优投资策略; Schmidli[2 ] 研究了在扩散和复合泊松风险模型中最小化破产概率目标下的动态最优比例再保险策略; Promislow-Young [3 ] 在最小化破产概率下探讨了最优比例再保险-投资问题; Yang-Zhang[4 ] , Lin-Li[5 ] 和 Li[6 ] 考虑了跳扩散风险过程保险公司的最优投资策略问题; Bai and Guo[7 ] 在无卖空约束下获得了多种风险资产模型中的最优投资策略; [8 ] 探讨了保险公司考虑负债情况下的最优投资策略. 关于此方面的研究还有很多, 比如: 考虑注资或分红下的最优控制问题 (文献 [9 14 ]); 通胀风险下的投资组合问题 (文献 [15 18 ]; 时间不一致下的最优策略 (文献 [19 ,20 ]); 相依风险下的相关研究 (文献 [21 24 ]); 方差保费原理下的最优决策问题 (文献 [21 ,25 27 ]) 等. ...

A quartet of semigroups for model specification, robustness, prices of risk, and model detection

1

2003

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

Robust optimal control for an insurer with reinsurance and investment under heston's stochastic volatility model

1

2013

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

Robust reinsurance contracts with uncertainty about jump risk

1

2018

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

Minimizing the probability of lifetime ruin under ambiguity aversion

1

2015

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

Robust optimal investment and reinsurance of an insurer under variance premium principle and default risk

2

2017

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

... 本节通过一些数值模拟来分析模型不确定下保险公司的最优投资-再保险-巨灾债券发行策略, 揭示关键因素对其的影响. 参考文献 [32 ,40 ,42 ], 本文参数取值见表 1 . ...

1

2010

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

A dynamic mean-variance model of portfolio selection under parameter uncertainty

1

2010

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

非线性期望理论与基于模型不确定性的风险度量

0

2015

Non-linear expectation theory and risk measurement based on model ambiguity

0

2015

Robust equilibrium reinsurance-investment strategy for a mean-variance insurer in a model with jumps

0

2016

Robust optimal portfolio and proportional reinsurance for an insurer under a CEV model

0

2016

Optimal investment and premium policies with ambiguity aversion

0

2020

不完全信息和模糊厌恶下 DC 型养老金最优投资策略

0

2022

Optimal investment strategy for a DC pension with incomplete information and ambiguity aversion

0

2022

Portfolio selections for insurers with ambiguity aversion: minimizing the probability of ruin

3

2024

... 然而, 模型不确定性是保险公司在实际决策中不可忽视的重要因素. 由于金融市场和保险市场的复杂性以及未来事件的不确定性, 保险公司难以准确知道自身的概率测度. 因此, 在最优投资-再保险策略中考虑模型不确定性显得尤为重要. Anderson[28 ] 提出了一种稳健控制方法来处理模型不确定下的建模问题. Yi[29 ] 和 Hu[30 ] 在模糊厌恶下研究了保险公司的鲁棒最优再保险和投资策略问题. Bayraktar[31 ] 则从终身破产概率的角度研究了稳健的最优投资策略, 并使用相对熵来描述两个概率测度之间的差异. Sun[32 ] 则进一步研究了存在模糊和违约风险下的稳健最优投资与再保险问题. 在模型不确定下研究的文献还有很多, 比如模糊厌恶下的最优投资再保险问题的研究(文献 [33 40 ]) 等. ...

... 证 请参考文献 [40 ,定理 3.1]. ...

... 本节通过一些数值模拟来分析模型不确定下保险公司的最优投资-再保险-巨灾债券发行策略, 揭示关键因素对其的影响. 参考文献 [32 ,40 ,42 ], 本文参数取值见表 1 . ...

Improving risk allocation through cat bonds

1

2004

... 特别地, 巨灾债券作为一种创新的风险管理工具, 允许保险公司将部分巨灾风险转移至资本市场, 从而降低风险分散的成本. 然而, 在现有的文献中考虑巨灾债券的研究相对较少. 据我们所知的相关研究有, Nell-Richter[41 ] 较早地研究了巨灾债券与再保险之间的替代关系, 发现巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力. Bauerle[42 ] 则在一个随机风险收入过程下研究了保险公司购买比例再保险和发行巨灾债券的风险管理策略. Li-Wei[43 ] 探讨了模糊厌恶下的巨灾债券发行和再保险策略问题. 研究表明, 巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力, 并能在随机风险收入过程下为保险公司提供有效的风险管理策略. ...

Traditional versus non-traditional reinsurance in a dynamic setting

2

2004

... 特别地, 巨灾债券作为一种创新的风险管理工具, 允许保险公司将部分巨灾风险转移至资本市场, 从而降低风险分散的成本. 然而, 在现有的文献中考虑巨灾债券的研究相对较少. 据我们所知的相关研究有, Nell-Richter[41 ] 较早地研究了巨灾债券与再保险之间的替代关系, 发现巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力. Bauerle[42 ] 则在一个随机风险收入过程下研究了保险公司购买比例再保险和发行巨灾债券的风险管理策略. Li-Wei[43 ] 探讨了模糊厌恶下的巨灾债券发行和再保险策略问题. 研究表明, 巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力, 并能在随机风险收入过程下为保险公司提供有效的风险管理策略. ...

... 本节通过一些数值模拟来分析模型不确定下保险公司的最优投资-再保险-巨灾债券发行策略, 揭示关键因素对其的影响. 参考文献 [32 ,40 ,42 ], 本文参数取值见表 1 . ...

Robust risk control with reinsurance and CAT bonds

1

2025

... 特别地, 巨灾债券作为一种创新的风险管理工具, 允许保险公司将部分巨灾风险转移至资本市场, 从而降低风险分散的成本. 然而, 在现有的文献中考虑巨灾债券的研究相对较少. 据我们所知的相关研究有, Nell-Richter[41 ] 较早地研究了巨灾债券与再保险之间的替代关系, 发现巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力. Bauerle[42 ] 则在一个随机风险收入过程下研究了保险公司购买比例再保险和发行巨灾债券的风险管理策略. Li-Wei[43 ] 探讨了模糊厌恶下的巨灾债券发行和再保险策略问题. 研究表明, 巨灾债券在高触发概率的重大损失保险中具有替代再保险的潜力, 并能在随机风险收入过程下为保险公司提供有效的风险管理策略. ...

1

2006

... 其中 $f'(x)$ $f''(x)$ $x$ $V_2(x)$ [44 ] ) 为 ...

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}